15.05.2024 / 07:45

An Uncertain Regulatory Framework for Green Hydrogen

Energy Markets

In our #HydrogenHorizon opener, we explored the green hydrogen investment landscape, highlighting regions of significant investment, project diversity, and investment gaps. Despite the industry's momentum and substantial funding, regulatory uncertainties contribute to many project struggles to secure final investment decisions (FID), with a success rate of just 10-20%. The lack of clear market guidelines and specific hydrogen policies has further delayed project starts, with slow regulatory progress disrupting development.

To realize green hydrogen's potential, investors need a clear understanding of the regulatory environment, including aspects like production, transport, storage, and carbon pricing. This edition focuses on efforts to address regulatory uncertainty in the European Union (EU), aiming to close the gap between ambitious plans, FID, and project completion. We'll outline key emerging regulations and policies impacting the hydrogen sector, including:

1.Revised targets promoting green hydrogen use

2.New regulations for infrastructure, certification schemes, and market entry

3.Incentives for cleaner hydrogen projects through carbon pricing mechanisms

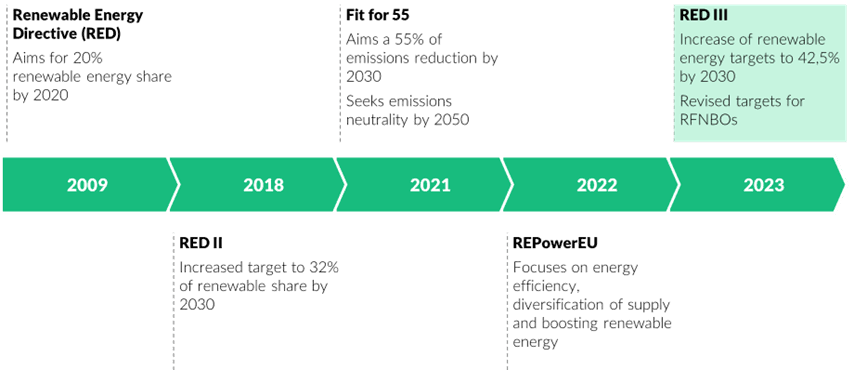

Renewable Energy Directive (RED)

The journey of the Renewable Energy Directive (RED) reflects the EU's escalating commitment to clean energy. Originating in 2009, RED aimed for a 20% renewable energy share by 2020. This goal expanded with RED II in 2018, targeting a 32% share by 2030, a target that became binding by June 2021.

The narrative advanced significantly with the "Fit for 55" package introduced by the EU Commission on July 14, 2021. This initiative, part of the European Green Deal, aimed to align the EU's climate legislation with its 55% emissions reduction by 2030 and 2050 neutrality goal. A key milestone was the revision of RED II, underscoring a deepened commitment to climate targets.

In response to energy challenges highlighted by geopolitical tensions, the EU launched REPowerEU in May 2022. Focused on energy efficiency, diversifying supplies, and boosting renewable energy, REPowerEU aims to cut fossil fuel dependence significantly.

The dialogue on RED II's revision led to a provisional agreement on March 30, 2023, culminating in the adoption of RED III by the Council on October 9, 2023.

Figure 1. Timeline of the Development of the Renewable Energy Directives

Updated RED III and Implications for Green Hydrogen

The RED III transforms the EU’s 2030 targets for the use of "renewable fuels of non-biological origin" (RFNBO), such as hydrogen or ammonia, methanol or e-fuels when produced from renewable hydrogen, in industry and transport into law. Beyond this specific focus, RED III broadly raises the EU's goal for renewable energy, aiming for a 10.5% increase (Figure 2) in renewables' share of final energy consumption by 2030.

The revised RFNBO targets also bring sector-specific targets (Table 1), clearly outlining the demand-side potential for the use of these types of fuels by 2030 and 2035. Member State countries will have 18 months to add these targets into their national hydrogen plans.

Table 1. Summary of renewed RFNOB Targets

Deal to decarbonize EU gas markets and promote hydrogen

The EU Commission in December 2023 endorsed an agreement between the European Parliament and Council to update EU regulations for decarbonizing the gas market and fostering a hydrogen market. Key highlights include:

Introduction of a certification system for low-carbon gases, including hydrogen, complementing renewable gas certifications in the revised RED directive, aimed at promoting fair competition in the Member States' energy mix.

Simplification of market entry for low-carbon gases by easing grid connections and offering tariff discounts for cross-border transactions, lowering costs for green hydrogen producers.

Enhancement of infrastructure planning for a decarbonized gas market, requiring development plans to incorporate electricity, gas, and hydrogen scenarios in alignment with various national and EU-wide plans, and to consider the repurposing or decommissioning of existing gas infrastructures.

Establishment of the European Network of Network Operators for Hydrogen (ENNOH) to oversee the planning, development, and operation of the EU’s hydrogen infrastructure.

Empowerment of consumers by aligning gas market regulations with those of the electricity market, facilitating supplier switching, providing price comparison tools, and ensuring transparent billing.

The provisional agreement awaits formal approval by both the European Parliament and the Council. Following this approval, the new law will be published in the Official Journal of the Union and will become effective 20 days afterward.

Carbon Border Adjustment Mechanism (CBAM)and Its impact on the Hydrogen Sector

The CBAM instrument intends to align the carbon pricing of imports to the EU with the carbon costs incurred by EU domestic producers within the framework of the European Emission Trading System (ETS). Specifically, its goals include:

Establish a fair price for the carbon emissions associated with the production of carbon-intensive goods imported into the EU.

Encourage cleaner industrial practices in non-EU countries to aid the EU's efforts towards decarbonization, and to avoid “carbon leakage”.

The CBAM mechanism will be rolled out into three phases: transition, review, and post-transitional phase.

The transitional phase (October 2023 – December 2025) serves as a learning period for all stakeholders, including hydrogen importers, and requires only the quarterly reporting of greenhouse gas (GHG) emissions without financial obligations or carbon pricing.

In 2025, the EU Commission will conduct a year-long review phase to potentially expand the CBAM's scope, using data from the transitional phase to assess expanding covered goods and refining emission calculation methods.

During the post-transitional phase (January 2026 onwards), only certified declarants can import CBAM-regulated goods, such as hydrogen, into the EU. Additionally, hydrogen importers are required to report volumes and emissions from the previous year’s in order to secure CBAM certificates.

The full implementation of CBAM is expected to start in 2034 with full effect in the initial sectors and goods, such as hydrogen.

Critique from the Industry

The introduction of regulations, frameworks, and definitions by authorities provide clearer guidance for hydrogen producers. While new regulations are welcomed by many in the hydrogen sector, concerns from others remain regarding the introduction of these new policies.

RED III presents both challenges and opportunities with its transformative policies and ambitious targets. However, Member States must effectively incorporate them into national law. The method for integrating these targets into national plans remains uncertain, potentially leading to further market fragmentation if the approaches to achieving these targets vary too greatly from one nation’s strategy to another.

In terms of the agreement to lower carbon emissions in the EU gas market, the European Network of Transmission System Operators for Gas (ENTSO-G) has expressed strong opposition to the inclusion of ENNOH, proposing that ENTSO-G, the European Network of Transmission System Operators for Gas, could fulfil its responsibilities instead.

Concerning the CBAM instrument, numerous industry stakeholders have raised concerns about adding hydrogen to the CBAM before evaluating its impact on other goods. Moreover, achieving the EU's hydrogen objectives requires reducing administrative burdens for importers, despite the additional regulatory complexity introduced by the CBAM.

Conclusion

European lawmakers are addressing key uncertainties in the development of the green hydrogen industry through their efforts, targeting specific concerns of project developers:

The revised targets in RED III establish legally binding goals for the inclusion of RFNBOs in key energy-intensive sectors, such as industry, transport, and the maritime sector, boosting the demand-side potential for green hydrogen.

Additionally, the agreement to decarbonize the European gas market sets clear regulations and frameworks for infrastructure, market access, certification, and sustainability to support the growth of the hydrogen market in alignment with the EU’s climate neutrality goals.

The introduction of the CBAM mechanisms impacts the hydrogen sector by pricing emissions from hydrogen produced outside the EU and imported into it, with the aim to encourage sustainable practices and reduce the carbon footprint.

Overall, these policies seek to provide more regulatory certainty and clarify the policy landscape for hydrogen project developers to reach FiD. However, the further deployment of these new rules and time will determine whether they achieve their goal or add another layer of complexity to the hydrogen industry.